Table of Contents

“I quit!”

There, you said it. Or you said it in your mind. You dreamed it again. You dream about starting a company and walking into your boss’s office and quitting your job.

What’s stopping you? Oh, about a million things including your mortgage and putting food on the table. You’re probably thinking, “I’m not rich. How in the world can I start a business?”

But you have an idea, and you’re sure it’s a good idea. How can you take your good idea and turn it into a company while you still have your day job?

I have worked with, invested in, and advised a lot of different founders as a venture capitalist, a founder myself, and a mentor to startups. I have also interviewed dozens of ‘mid-life’ entrepreneurs for my forthcoming book Never too Late to Startup. One thing I hear pretty frequently is from people with ideas who can’t figure out how to turn those into businesses.

Ready to start minding your own business? Here are 12 proven steps to starting a business while working full time:

1. Throw Away Your Business Plan!

If you have taken any business classes, or perhaps got an MBA, you almost certainly heard about a “magical” document called a business plan. Perhaps you even wrote one. I sure did when I got my MBA. When I was a venture capitalist, I read hundreds of them. It used to be startup gospel that you had to have a business plan.

The reality of the startup world is that business plans are obsolete only moments after you write them. Extensive market research doesn’t really help you come up with a great product that customers will love. Detailed financial plans will be wrong as soon as you change the price point, or the marketing channel, or the features.

But it’s not as though planning itself has no value. It does. It’s just that what your product is, what your value proposition is, and how you’re going to market and sell it, is likely going to change significantly after you start building and getting real customer feedback. The boxer Mike Tyson once said “Everybody has a plan until they get punched in the mouth.”

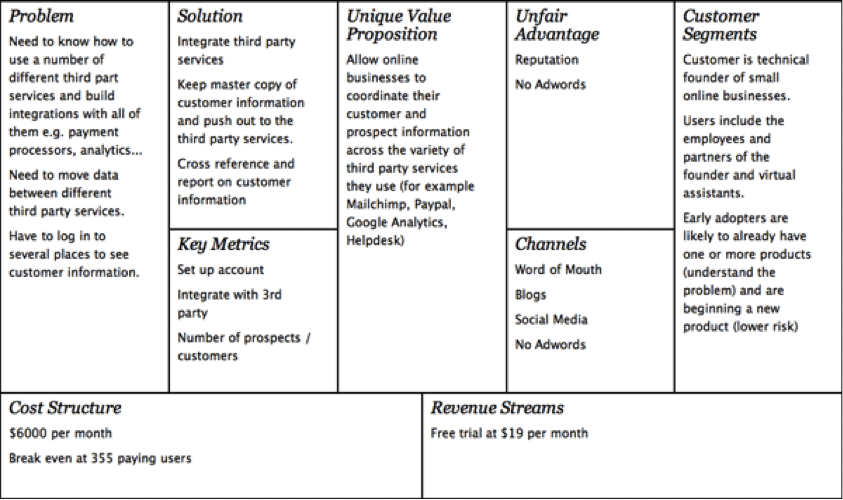

Instead of a business plan, I recommend using a 1 page document to list out your assumptions about the business. There are a number of templates out there to help you do this in an organized fashion. The most popular one is called Business Model Canvas, although I prefer a variant of it called Lean Canvas created by Ash Maurya (named after the so-called “Lean Startup” movement which emphasizes moving quickly and staying small until you have validated many of your assumptions).

Here is an example from Furld.com, a web based tool to help startups. (I have no affiliation with Furld.)

Any of these types of tools will do the job of helping you think through and write down your most important assumptions:

- What problem does your product solve?

- What is your product?

- Who are your target customers?

- What is really unique about it?

- How are you planning to distribute your product to customers?

- Where will your revenue come from?

- What are your major costs?

This type of plan is perfect if your have a day job, because it takes a lot less time than an old style business plan, and your time is precious.

2. Get Your Legal Ducks in a Row to Make Sure You Don’t Cross Your Current Employer

One thing you need to do is to make sure you are on solid legal ground so your employer can’t come after you when your startup is a raging success. The easiest way to avoid any trouble is to be sure you are working on an idea that is unrelated to the business of your employer, and to work on it on your own time and with your own equipment.

Look through your non-disclosure and other employment agreements to see what your company’s policies are. The law varies by state as to what your employer can and can’t ask of you. It also really depends if you are working on something that will compete with them, or something that came out of your work with them. Typically, both of those are no-nos. The other document to look at, if you signed one, is your assignment agreement. This says that your ideas related to your employers’ business belong to them.

You might want to consult with a lawyer. John Gilluly, partner at DLA Piper and one of the leading startup lawyers in the country, suggests that getting this wrong can result in getting fired, or in having your new company’s intellectual property be subject to claims from your employer. Make sure you go through these documents and this process so you don’t have to worry about any of that.

3. Look for Co-Founder Who Fits Like a Glove

Startups are tough, and they are even tougher when you try to do them alone. While there are plenty of examples of great startups with one founder, having a good cofounder increases your chances of success. Cofounders add to your company’s skills, they share the workload and improve company productivity, and they are someone with whom you can share the emotional burden.

Don’t take my work for it. Reid Hoffman, founder of LinkedIn and investor in tons of successful companies recently said:

“Most often two or three people is much better. When I look at these things as an investor, and I say ‘What is a good composition of a project and founders that are likely to succeed?’ It’s usually two or three of them.”

That said, cofounder disagreements are one of the leading causes of startup failure. So what to do?

Think about it like a marriage. Try to start your company with someone you know you are compatible, preferably someone you have worked with before. If that’s not possible, think about a “try before you buy” arrangement where you both “test things out” during your night and weekend work.

And always, always put in place a vesting schedule for equity in the business so if your cofounder decides to leave (or any employee for that matter), they don’t take a large chunk of the ownership of the company with them.

But don’t delay starting your company because you can’t find a cofounder. You’re better off starting, getting some momentum, and then finding someone. It will probably be easier that way, anyway, since your cofounder will see the progress you have made.

4. Test Your Idea Like Crazy

Just because you have a great idea does not mean the market is going to agree. You already listed out your assumptions in the Lean Canvas exercise above. Now it’s time to put those assumptions to the test.

Testing your idea rigorously is the best way to reduce startup risks. Doing this while you’re still working is a little tricky, and time consuming, so it’s going to require thought and planning. Here are a couple ways to begin:

1. Customer Interviews: As startup guru Steve Blank preaches, you need to get ‘out of the building’ to interview your prospects and see if they actually have the pain/problem that you think they have. You can find out a lot from these interviews. Try to learn how big the problem is to them, how they would use your product/service to solve it, how entrenched they are in their current way of solving it, and what it’s worth to them to solve it a better way.

2. Prototypes: The goal of a prototype is to deliver the bare minimum product that meets the highest pain point of your customer. In startup lingo, this is called an MVP, or Minimally Viable Product. Keep it inexpensive at this point. The goal here is to get user feedback so you can change the product. The most important thing at this stage is to keep an open mind. The customers may not share your vision–you need to meet them where they live. After all, they’re the ones who matter.

A good example of this is Van Barker, who spent decades in corporate America working for companies like Hewlett Packard and Pepsico before founding Yardstash, an outdoor bike storage company, as a side project. He was able to get it to over $250,000 in sales through eCommerce before quitting his day job.

For Van, the prototype process allowed him to significantly improve the product. “With our prototypes, I got them in the hands of bike owners and learned a lot. We were able to use the feedback to improve the quality, and we changed the design to make the units easier to assemble. The next design cost less to make as well.”

3. Surveys: Surveys are a great way to reach hundreds or even thousands of prospects. Surveys are a extension of customer interviews because it’s hard to interview enough customers. Tools like SurveyMonkey make it super easy to run a survey and get analysis of the results. Unlike in interviews, you want to ask more ‘closed’ questions with a range of numerical answers, and don’t pitch or sell in the survey. Use a 5 point or 7 point scale, so respondents can answer on a range. It makes it MUCH easier to find patterns in the answers.

Example of Bad Survey Questions:

What do you think about XYZ idea?

Tell me about your problems with medical paperwork.

Examples of Good Survey Questions:

Do you file your medical bills?

- Never, I don’t even open them

- Sometimes.

- I try to but sometimes I can’t get to it

- Almost always

- Always. I make a point to do it

4. Use the Interactivity and Reach of Internet: It is pretty easy to set up a basic web site and test your concept very inexpensively on real live prospects. You can use an inexpensive product like LeadPages to set up a few different descriptions and see which ones customers like more. You should also use Google Adwords to see if people are using Google to search for answers related to your startup. This is a good sign, because it means there are customers out there for you. You can test advertising on AdWords or Facebook to see if you can get consumers to click. This can be a good proxy for how much it’s going to cost you to get new customers.

5. Don’t Make This a Hobby

All of us have hobbies like cooking, gardening, Yoga, reading, dancing, etc. But I can’t think of anyone who sets goals with their hobbies, with targets and deadlines, and tries to rigorously adhere to them.

To turn your idea into a thriving business, you need to set goals for your startup and hold yourself accountable to them. Plan out your next steps, with dates and specifics as best you can. This is one more reason why it’s helpful to have cofounders, since you can help hold each other accountable.

I get it- you have a busy life with a job, family, kids, book club, etc. It’s way too easy to put off the work on your business until tomorrow. Setting concrete goals like “Write Web site copy by next Tuesday” or “Interview 10 customer prospects in the next 30 days” will help you get past that natural inclination to put things off.

I am NOT suggesting that you try to create a detailed plan for everything for months and months. There is simply too much that you don’t know for that to work. But knowing the next few steps, and forcing yourself to get it done on a time schedule, will create positive momentum and also will create clarity about the steps that follow. As noted entrepreneur and former corporate CEO Michael Hyatt says, “We only begin to get clarity when we get in motion.”

6. Don’t Be a Scrooge

Your natural instinct might be to save aggressively in preparation for the time when you are full-time on your startup and you have a much lower income. Certainly many financial experts will tell you to do that.

I think about it a little differently. I think you should take any extra money you have and invest it in your startup. Spend some money on Google Adwords and start building an email list. Get some inventory of your new product. Get professional business cards. Attend networking events. Hire a virtual administrator.

Obviously, you don’t want to go crazy here and waste tons of money. But small investments to get your business moving faster—generating more revenue, building your network, getting good legal counsel or patent protection, setting the stage for this business to be viable and support you and your dreams- these are good investments.

Good investments: Anything that helps you get your idea to market quickly & grow your customer base

- Basic URL and web site

- World class people, either full time or contractors

- Surveys, interviews, and prototypes to get closer to understanding whether the market wants your product/service

- Marketing that brings in interested customers and is testable (like Facebook, Google, Twitter)

- Legal counsel (expensive but worth it)- See if you can get discounts

Not so good investments: Most other things that you can avoid, penny pinch on, or defer

- Overhead like rent (work out of your house), furniture, expensive computers, travel (unless it’s to see prospective customers)

- Branding

- Expensive logos

- Market research studies / reports

- Accountants (your numbers are simple, use Quickbooks)

7. Start Generating Revenue

If you have done your homework and spoken with enough customers, you will find customers willing to pay you for your MVP or a variant of it.

Paying customers changes everything. It takes you past the “Yeah that sounds like an interesting solution” to “I’m willing to pay you for your solution to help solve my problem.” Once you have paying customers, you can ramp up marketing and sales by looking for more like them. You might be able to use your early customers as testimonials. They might even refer you to other prospects.

Trust me, emotionally, there is almost nothing that makes you believe that “This can be a business” than paying customers. And eventually, you’ll have enough of them for your business to support you and let you get rid of your day job.

8. Network Like Crazy

Use the fact that you still have a job as fuel to network like crazy. Having a job is great, because you interact regularly with other employees, customers, vendors, even competitors.

Network inside the company as well as outside. Try to meet people who can be potential employees, potential customers, potential contractors, potential advisors and mentors, and potential investors.

These connections are all potentially valuable. You know how it goes with networking: you’ll meet someone who knows someone who is looking right now for a solution to the one your startup will solve.

Do not overlook the idea of finding mentors now, before you need them. Those could be formal relationships, or they could simply be people you will call when you have a question that they can answer.

9. The Secret to Why You Don’t Want Investors

It’s not that you don’t want investors ever, it’s that you don’t want investors yet.

When I was a venture capitalist, we used to see founders with good ideas who wanted investment so they could quit their jobs and pursue their business. I understand the logic, it makes sense.

But to the investor, if you have not moved the business along, tested the concept on real customers, built a prototype, or tested your marketing assumptions, you simply don’t look serious. Investors almost always want to see you working full time on the business so they think you are maximizing their chance to get a return on their investment.

Even if you could get investors interested, your lack of traction would put a very low value on your company at this point. So low that you would need to give up a very large piece to the investors.

Finally, there is your time to consider. This isn’t like Shark Tank, where you show up and pitch. The process takes much longer than that to identify the right investors, to pitch them, and to go through their due diligence process. You are much better off at this point using that investment in time to move your business forward.

10. Make Your Nights and Weekends Count

I think it was Oprah Winfrey who said, “You can have it all, just not all at once.” This is the perfect quote for the time when you’re pulling double duty in your day job and building your startup. If you have other commitments, like kids or a spouse, it can feel like triple duty.

If you’re starting to see traction in your startup, now is the time to make those nights and weekends count. I’m not saying drop everything, but be willing to make some tradeoffs so that you can meet your goals. Your time is your most valuable resource right now, so use it wisely.

The reality is that this might be the time to put some things on the back burner. For these next six months, you might not be able to coach soccer, or take a long vacation, or do your regular poker night or book club.

If you find yourself getting stuck, as many of us do, just try to keep things moving. You can get yourself unstuck by only focusing on the next step. Break down the problem, write it out, and use baby steps to get yourself moving again.

11. Act Like A Big Company even When You Have No Employees

It’s easy to think that you are a 1 person business (or 2-3 person if you have some cofounders or employees). But the outside world doesn’t know how big you are, only that you have a product/service they are interested in. It is important to project a professional image about your company in terms of your web site, your customer service, your fulfillment, your appointment setting and your follow up.

You can find freelancers who can help you to test the concept, and to execute on it. It’s all there on the Internet. If you need freelance programmers- try oDesk or eLance; outside suppliers or manufacturers- try Alibaba; graphic design or marketing- try 99designs or Fiverr; personal assistants to answer phones, set appointments, or book travel- try eaHelp.com, GetFriday, or Brickwork; eCommerce fulfilment- try Fulfilment by Amazon; general tasks and To Dos- try TaskRabbit or Amazon Mechanical Turk.

The bottom line is, you can use these outside services to manage a pretty extensive operation without YOU needing to do it all. This will enable you to grow the business to a sufficient size that you can consider quitting your job.

12. Jump In Full Time (and Quit)

If you have taken all of these steps, you have a growing business that has launched a basic product or service. Starting a business while working full time is much different than running and growing a business while working full time. You have paying customers and a good idea of how to market and sell to find more. You have tapped your network for help and you know your go-to mentors and advisors. And you’re using virtual resources to help grow your business and project a larger more professional company to the outside world.

When is it time to quit your job and go full time on your startup? It’s probably before you’re ready. The right time is probably once you have proven that you can deliver a product or service that customers want. It’s likely before you can replicate your full day job salary, but when you have line of sight as to how that will happen.

As Michael Hyatt says,

“It’s not when you feel comfortable. At some point you say, I’m going for it.”

Wrapping This Up…

It’s easy to read a list like this, but really, really hard to actually do it. I know it feels like you need more time and a bunch of money to start a business.

You don’t.

Achieving your dreams requires work. It will take time, energy, dedication, and courage.

Close your eyes and think about your “I quit” moment or about walking into your new office with your company’s name on the door.

Now open them again and start planning your future as an entrepreneur.

Great tips, thanks! I especially liked the part about testing your idea. I know about this firsthand, as I do business on Amazon. I have 3 years of experience, so I know that this business has its own nuances.

For example, one of my tips for getting started is to join the Amazon community to get relevant and current news. That tip can be helpful for all types of businesses, I guess!

Hi Rob, I a Citizen of Kenya living in Nairobi and I have been Struggling with the Idea of setting a Company to Manufacture TV Aerials. Despite my efforts to reach out both at Home and beyond to seek Funding, I haven’t succeeded due to factors such as Not having Registered my Business , Lack of Assets for Security and my Country Kenya not being Covered in the Network of the Global Funding Platforms.

The Few Aerials that I have so far made Manually and brought into the Market have served exceptionally well. Please advice me on how I can Turn my Idea into Reality because I don’t have a Penny in Savings.

Simon Ojiambo.

Should I focus towards registering my company and other stuff or just start with my business and register later. And if later then when?

Depends on where in the world you’re located because laws are different in every country. But remember one thing, if you don’t have customers you don’t have a business. So I would suggest getting customers first and then once you have a business that make money, register your company.

This is the best thing I’ve ever read on the internet yet about starting whilst in full time employment.

Down to earth and to the point.

Saved in my favourites!

This has given me the kick up the backside I needed.

Much appreciated (:

Hey Rosie that’s awesome! I love it and thanks for reading. If you ever need anything make sure to reach out 🙂

Very useful tips, these points are always helpful in order to starting a startup. Thanks for sharing.

Thanks for checking out the article!

This is such a good article. We also have some ideas on how to start a business

I am a Registered Nurse of 11 years with a Lean Six Sigma Black Belt. Most of my process improvement experience is within the Emergency Department and I would like to start a consulting business on the side. How would you recommend I begin this journey?

Hey Jeanne, you have some awesome experience! You can totally make that a full time consulting business. You need to make a list of all the hospitals and emergency centers within 1 hour of where you live. And then one by one talk to the hospital administrators or director and tell them how they can save more money, more lives, and increase capacity…etc with your help. Hospitals are always looking to cut costs and if you are able to save them money then your contract would pay itself. It will be a slow roll to get started but if you talk to enough hospitals eventually they will start saying yes.

Hello sir thanks for the guide us I am new here and started a blog for home base income this article give me new energy such a great and educational post

Hi Rob, I have couple of questions regarding the process of starting up a company while working as a full time employee.

1. How can I register the company, .com domain, etc… when I am working with a employer which has strict rules about not doing when I am in this firm?

2. How can I really develop a MVP and take it to customers to analyse the idea, if it is working, can I continue to accept the revenues even when I am working? Again, where to accept the payments?

3. What if all co-founders are working employees and want to startup a company/business?

Basically, we want to start a company, when working with another employee, try our idea in the market, if it is working well, accept some revenue, quit our jobs when we have good business with our idea.

Could you please suggest the best ways/options that we can follow in this situation.

i think you could always register your domain in a different name (with a potential partner of your who need not necessarily from your line of business) till you gain a momentum on the ground.

Thanks for the tip Samy!

Thank you Mr Rob,am a Kenyan guy recently working in Mombasa town.I prepared my business plan while undertaking my diploma course,much honour for reminding me where my actual business life could begin.

How to run multiple business along with a full time job.

Awesome and close to practicalities every startup faces

I’m Mrs.Mariejo Mortega by name. I live in United States Maryland, i want to use this medium to alert all loan seekers to be very careful because there are scammers everywhere.Few months ago I was financially strained, and due to my desperation I was scammed by several online lenders. I had almost lost hope until a friend of mine referred me to a very reliable lender called Mr. Peter Jackson who lend me an unsecured loan of $650,000.00 under 24hours without any stress. If you are in need of any kind of loan just contact him now via: [email protected] I‘m using this medium to alert all loan seekers because of the hell I passed through in the hands of those fraudulent lenders. And I don’t wish even my enemy to pass through such hell that I passed through in the hands of those fraudulent online lenders,i will also want you to help me pass this information to others who are also in need of a loan once you have also receive your loan from Mr. Peter Jackson, i pray that God should give him long life.

God bless him forever.

Mariejo Mortega

Testimony on how i got my loan

The first point made me smile. So true. Sometimes a business plan, no matter how well-written it is, will have to be thrown out the window the moment something changes. And change is the only constant in this world.

Rebecca- Thanks for your comment. Yes change is certain and that’s why I think “business plans” should really be about documenting and testing your assumptions. In my opinion, everything else (market size, detailed projections) is just noise until you validate some of those assumptions.

Eisenhower said, “In war, plans are meaningless. But planning is indespensible.”

Thank you so much for the great article! I thought you might enjoy this post we recently wrote about how to find time for your business when you are working full time!

This is an awesome article Rob! I am currently in the middle of building my business while still working a corporate job, so I know all about the late nights. I love the idea of creating a one page document instead of a full blown business plan. I will be checking out Lean Canvas shortly. Keep up the great work !

Steven- Congrats on starting and building your side business. Best of luck to you. I’m going to do a post soon on a 1 page business plan.

Steven- here is the link to my free 1 page business plan guide http://www.startlaunchgrow.com/1-page-business-plan

Very useful information. I am just preparing my business plan and setting up goals for my startup. Parallel, I am developing my product to enter into the market perhaps by collaborating with near and dear friends and organizations. Expecting more articles from you in this line to educate my self.

Its a very tough to continue the day job and working on my plans during nights and weekends without getting disturbed from personal life from my children and wife. But I am strong on my determination.

Srinivas- Thank you. Best of luck to you. Your determination will be a big factor in your success!

Thank you for this useful and well-written post Rob. My takeaway: Practice patience and persistence. 🙂

What useful information Rob. I have a hard time deciding what point is my favourite, so I won’t bother. Just know that I’ll be looking for more from you!

As I embark on my new business, finding the time to do the work is a real challenge. With a toddler in the house, the only quiet time I can get any real work done is when everyone’s gone to sleep. So, I definitely know what it means to make my nights count. The difficulty has been deciding what to put on the back burner which, for me, leads to analysis paralysis. What finally helped me to get unstuck is a quote which said that “if you procrastinate, you haven’t sold yourself on it yet.” A lightbulb went off.

I was stuck because I wasn’t totally convinced of a particular idea or course of action. It’s a sign that I needed to do something different. But once I got clarity on my ideas, I became much more productive and energized. And it wasn’t such a struggle anymore to stay up every night until 2 a.m. to get the work done.

Jeanne- Good luck on your new business. Tricks to get “unstuck” are worth their weight in gold.

Great article Rob. You make really solid points.

I have another perspective on business plans. What is valuable about them is not the finished plan, it’s the research process you go through to create a finished plan. This process adds invaluable intelligence that helps you build a better startup.

Sure through away the finished plan, but don’t throw away the process.

Susan- Thanks. I agree the process is valuable. I am trying to highlight that there is an easier way to get going on that research that hopefully won’t be as daunting to a first time entrepreneur.

Hi Rob,

The Mike Tyson quote made me laugh out loud. So true! And I was pleased to see you recommend the one-page Business Model Canvas. It’s a fantastic tool that completely helped me to be laser focused. Much more so than the traditional business plan model. Right on!

As an entrepreneur with several successful business start ups under my belt, your advice is right on target! Wish I’d read this before I learned things the hard way!

I like having the Legal Ducks in a Row, it would be disastrous to have your brand brought down for careless mistakes. Good read.

Great tips Rob. Never thought I’d read about Mike Tyson and business plans in the same article. And clever use of his quote “Everybody has a plan until they get punched in the mouth.” LOL. When can I get a copy of your book?

Helen- Thanks. My book will be out mid-year. In my case, I’m working full time, and working on my book and my side business, so it’s taking a little longer. Not complaining! I wouldn’t have it any other way.

Loved #6! Great advice on the best places to invest your money before you think about quitting your job. I find the many choices out there overwhelming, but your list makes perfect sense!

Nicki- I think about the possible investments just like I think about my time- what small investments will have the biggest returns.

Ok,

I also started my first business while still working in corporate.

It was not easy. But, it was worth it.

I had to cut down on some other “social” time, but it was all worth it. I ended up quitting my job just under 6 months later, and moved to Latin America to baseline expenses as I got things underway.

Well said, Rob. Don’t make it a hobby. Treat yourself as your #1 client. Value the crap out of your time (make those nights and weekends count), and get to work!

This is great advice Rob – Number 2 especially struck a chord with me, as so many people start up a business without checking their contract which often says they’re not allowed, or need permission, or worse, that anything they create might belong to that company! Really good article.

Thanks Ellen. It’s sad when you see people in disputes with their former employer. It’s not that hard to separate the startup intellectual property, but you have to make sure it gets done.